The bond market, also known as the debt market or the fixed-income market, refers to the marketplace for issuing and trading credit securities. The bond market has a history as rich as the stock markets and has come a long way through various developments. Here is a chronicle of the bond market history and the significant events that have led to its evolution.

Bonds are one of the oldest forms of financial instruments dating back to the Mesopotamian ages. Over the years, it has emerged as one of the most sought-after ways of raising funds by government and large corporations. Bonds are over-the-counter fixed-income instruments that the investors purchase for profits and to protect their portfolios.

The bond market in the United States comprises several kinds of issuance, primarily the Treasury. With the rise in credit demand, other forms such as the municipal bond market, corporate bond market, and the most recent derivatives market emerged. Before World War II, the corporate and municipal bonds market was active on the New York Stock Exchange. However, in the late 1920s, the demand for municipal bonds plunged dramatically, while in the mid-1940s, corporate bond’s demand went downhill.

The debt securities market went through various advancements over the centuries. The global bond market stood at $123.5 trillion in 2020 as per the Securities Industry and Financial Markets Association (SIFMA).26

In this article, we take a look at the rich history of bond investing.

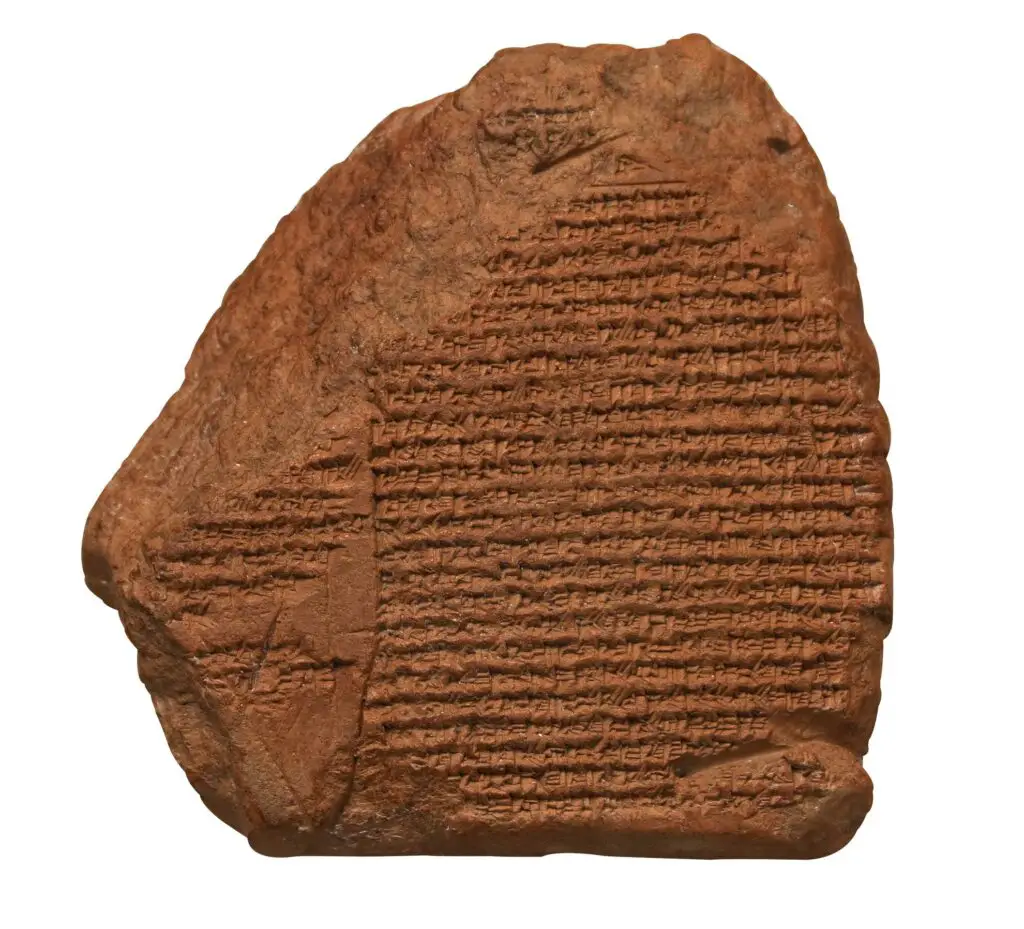

2400 BC: Ancient Bonds

The first evidence of a bond with a legal binding dates back to 2400 BC. Archeologists discovered a stone tablet from an excavation site in Nippur, Mesopotamia, or present-day Iraq, which looks like a standard surety bond. The surety bond guaranteed reimbursement in case the principal failed to make payment.1 Currently, the stone tablet is preserved in the Pennsylvania Museum of Archaeology.

The principal used this bond as a guarantee for the payment of grain or reimbursement if he failed to make a payment. This was the time when corn was the official currency.

Another region that issued government bonds in early 1100 was Venice. The money was called Prestiti and was used for war funding. Most of the affluent Venetians began investing in these bonds.2 This was a part of one of the earliest bond markets in the history of Europe, where the prestiti was seen as an important innovation. Those who invested in prestiti were paid a nominal interest rate of 5% per annum. In his novel, A History of Interest Rates, author Sydney Homer has discussed the evolution of bond markets of Venice in detail.3

In 1214, Genoa’s public debt was divided into shares of 100 lire and was called luoghi or loca in Latin. These shares or luoghi were transferable and standardized and also resembled the present-day government bond.5

The royal families of England and France failed to pay off large debts to Venetian bankers post the Hundred Years’ War, causing a collapse of the Italian banking system, also called the Lombard banking, in the 14th century.

This resulted in a substantial economic setback impacting every sphere of life. The plague called Black Death that followed spelled a complete disaster for the European economy. The bond market was wholly depleted, and there was a ban on bankers trading government debt.

1693: The First Official Government Bond

In 1693, King William III of England sought a massive war fund to fight a battle against King Louis XIV of France.4 This was precisely before the Bank of England came into existence. The parliament was in its initial stages of figuring out new borrowing schemes. It decided to borrow the money from the high net worth investors in London and overseas. This was very similar to what we call government bonds.

The Exchequer paid annual coupons of 7% semi-annually to the investors. However, in case of the death of the investor or bond buyer, there was no option for him to pass it on to a family member or loved one. The benefit would stop if the investor passed away.

1775: The US Used Bonds to Finance the Revolutionary War

After the 16th century, more countries followed England, and bonds became the most preferred war funding.6 Soon, other countries started following, and the US government used bonds to finance the Revolutionary War or the American war of Independence in 1775.

The Treasury offered loan certificates whose structure was very similar to bonds. During that time, private individuals bought bonds worth over $27 million to finance the war.

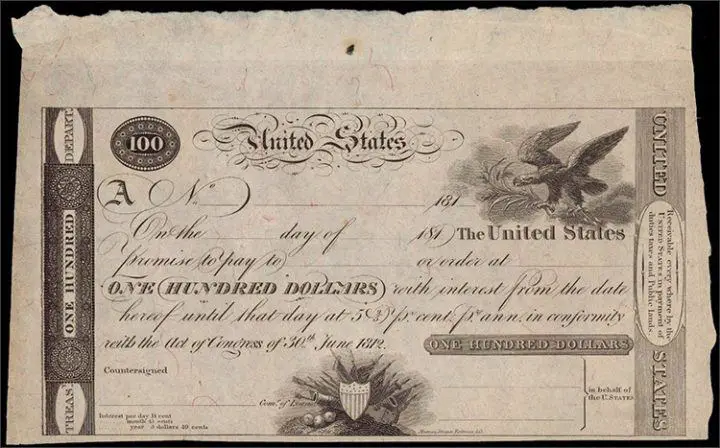

1812: The US Issued War Bonds Worth $11 Million

The term “war bond” was first used when the US Congress issued bonds and raised A recession$11 million to fund the War of 1812.7 However, it was not intended for the general public. America jumped into war without any kind of funding strategy.

The usual sources of government revenue, such as customs and land sales, dried up due to the sales. The federal taxation of incomes was put on hold in 1811, because of which the government had to resort to loans and credit. The government now began to access banks and affluent merchants for raising capital. In June 1812, Congress authorized the first U.S. Treasury Note to fund the War of 1812.

By the spring of 1814, Congress had authorized then-President James Madison to borrow $32.5 million to finance the war as the climate for the US Treasury bonds began to dampen.8

1812-1842: The Rise of Municipal Bonds

Municipal bonds are issued by the state and local governments to raise capital for social infrastructure projects like schools, healthcare centers, roads, bridges, etc. These bonds made an appearance during the Renaissance period in Italy.

Still, it was officially launched in 1812 when New York City issued a general obligation bond for the Erie canal project.9 There were 42 different bond issues to fund the project over the next four decades. After 1840, many American states were in debt, and by 1843, the total debt crossed $25 million.

After the American Civil War in the 1860s, there was significant local debt issued for railroad expansion. However, after the panic of 1873, several local governments defaulted, and the issuance of municipal bonds was halted.

1914: The Issuance of Austro-Hungarian Loan

During the early days of World War II, the government of Austria-Hungary implemented a war funding policy on the lines of Germany. In November 1914, Austro-Hungarian issued a loan at half-yearly intervals in November and May with a prearranged plan. The first Austrian bonds had a five-year term that paid 5% interest, and the smallest bond denomination was 100 Kronen.

After its separation from Austria, Hungary issued loans separately in stocks offering an option of repayment to subscribers after a year’s notice. The interest rate was 6%, and the smallest denomination was 50 korona. Subscriptions to the first Austrian bond issue were worth $440 million, while those of the first bond issue in Hungary amounted to $235 million.

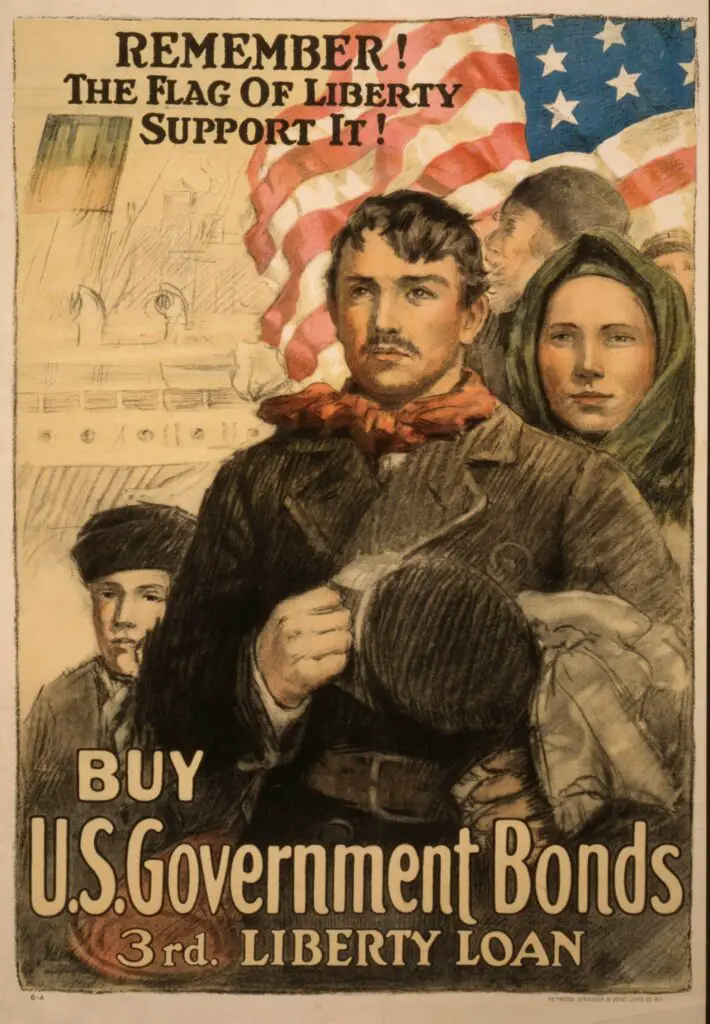

1917: The Issuance of Liberty Bonds

In 1917, the US government-issued bonds worth $5 million at a coupon rate of 3.5% as war funding against Germany during World War I. The rate was lower than what typical savings account offered at that time.10

These U.S. Treasury bonds were also called the Liberty Bonds and were issued in four installments between 1917 and 18. These bonds were created under the “Liberty Loan” program launched in 1914 due to a joint venture between the US Treasury and the Federal Reserve System.

Congress launched the Liberty Bonds under the Liberty Bond Act, later called the First Liberty Bond Act. This is because there were three more acts for authorizing additional bond issues during the war. There was also a fifth round of the act to authorize bond issues in the post-war period.

Through the Liberty Bond program, the Americans helped the Government raise money for the military operations. In return, the government also promised to return them the money and a specific interest rate after a few years.

The federal government encouraged US citizens to invest in the bonds to showcase their patriotism and support its military. However, Liberty Bonds received a lukewarm response when first issued in April 1917, leaving the Treasury Department disappointed.

To ensure more success during the second offering of Liberty Bonds in late 1917, the government organized an extensive public awareness campaign coupled with other promotional tactics.

While the first issue of Liberty Bonds had a 3.5% coupon rate, the interest rate gradually increased up to 4.25%. Still, the government appealed to citizens to invest in these bonds primarily for patriotism and not profit.

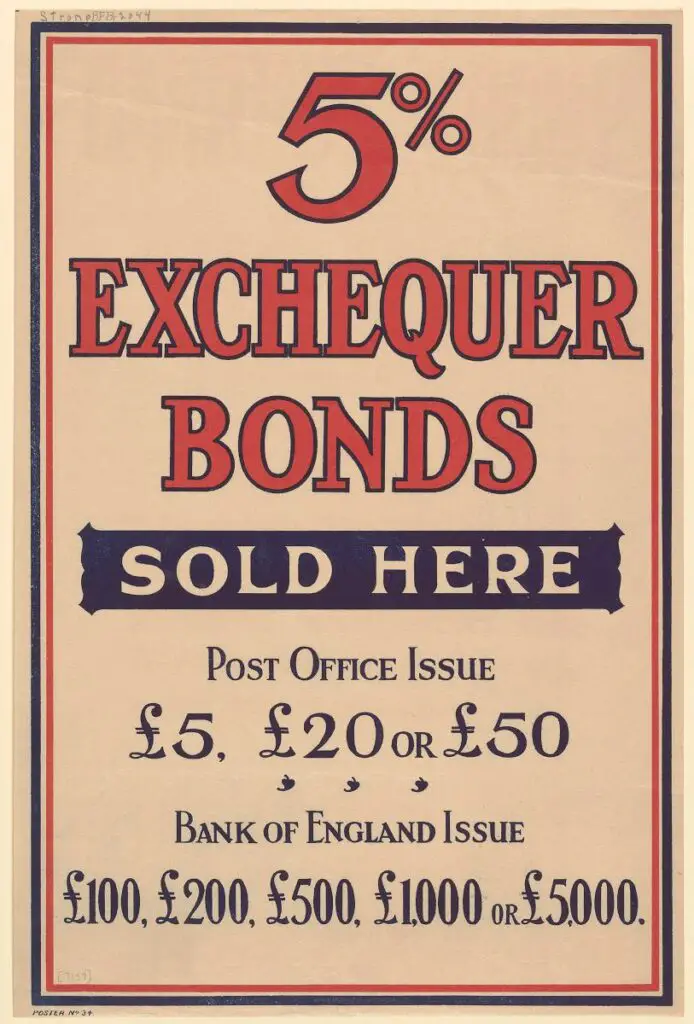

1917: UK Bonds Financed First World War

In 1917, the British government issued national war bonds with a coupon rate of 5% to raise more capital. These bonds were sold to private investors with a massive public campaign that said: “If you cannot fight, you can help your country by investing all you can in 5 percent Exchequer Bonds … Unlike the soldier, the investor runs no risk.”12

Most small investors purchased these bonds. 92% of holders owned less than £10,000 each of the bonds, while 7,700 investors held less than £1000 nominal value.

1917: The Canadian Victory Bonds

Canada began to issue war bonds in November 1915, and they came to be known as the “Victory Bonds” after 1917. The First Victory Loan offered an interest rate of 5.5% in $50 denominations. Because of its smaller denomination, it was quickly oversubscribed and raised over $398 million.

In 1918 and 1919, the Second and Third Victory Loans were floated, which raised an additional $1.34 billion. Many could not afford the Victory Bonds, so the government issued War Savings Certificates. The communities who purchased large amounts of Victory Bonds were given Victory Loan Honour Flags.27

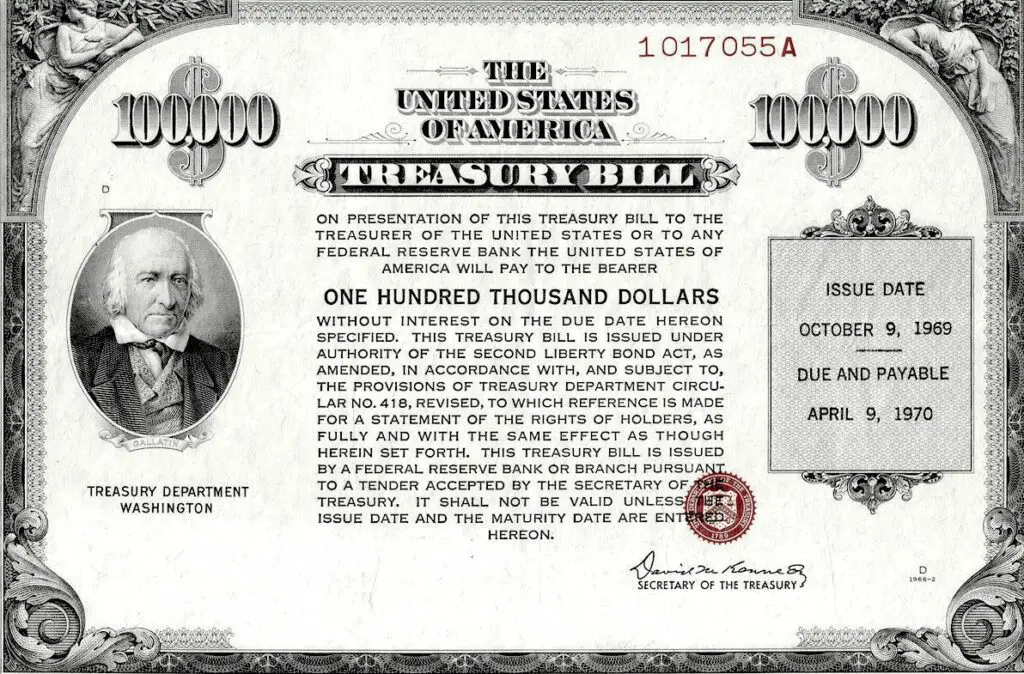

1929: The First T-Bill Auction

In the 1920s, the U.S. Treasury financing operations reflected several flaws due to fixed-price subscription offerings practiced during war times and restricted Treasury debt sales frequency to quarterly.

To plug in these loopholes, the Treasury introduced the Treasury bills. The US Treasury was not authorized to modify the financial structures of the government or introduce new instruments. Therefore, President Herbert Hoover signed formal legislation to incorporate new security called T-bills.13,15

From 1929, Treasury bills started getting auctioned instead of being put up for sale at a fixed price. They were also sold on demand instead of on a quarterly frequency. This also addressed the growing need for gilt-edged investments.

These auctions became regular occurrences, and their yields to maturity became the standard ‘risk-free rate’ for other credit purposes.

During the stock market collapse in 1929, the long-term government bonds, which returned 3.4%, were seen as a safe haven. The equities performed miserably during the Great Depression.

However, the US bonds saw impressive returns during this phase. Bond bond prices were rising while the bond yields began to slide. After this point, even other corporate and municipal bonds could systematically create a yield based on the credit terms.13

The prime corporate bond yield average dropped from 4.59% in September 1929 to 3.99% in 1931. In 1938, the average corporate bond yield reached a low of 2.94%. However, due to deflation, many cash-strapped corporations and municipal governments defaulted on their debts in 1930, and fixed-income investors incurred huge losses.

Two Wall Street investors that earned massive profits after the Crash were Alfred Lee Loomis and Landon Thorne, his partner and brother-in-law. Both were leading financiers for the electric power industry in the 1920s. Alfred Loomis was also a scientist.

By early 1929, both these partners had liquidated their entire equity portfolio and invested the profit into long-term Treasury bonds and cash.14

Jennet Conant, author of Tuxedo Park: A Wall Street tycoon and the Secret Palace That Changed the Course of World War ll, stated, “in the midst of so much despair, with the economic situation deteriorating day after day, Loomis and Thorne continued to profit handsomely.”16

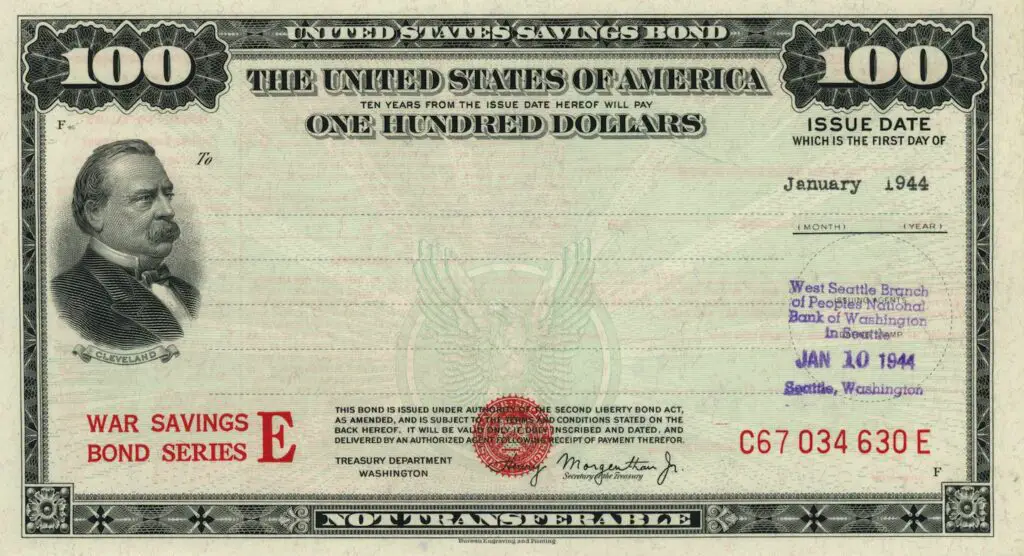

1935: Launch of the US Savings Bond

On February 1, 1935, President Franklin D. Roosevelt passed legislation allowing the U.S. Department of the Treasury to launch the U.S. Savings Bond for sale. Within a few weeks, the first Series A Savings Bond was issued. With a low purchase price of $18.75 and a face value of $25, the bond was nicknamed “the baby bond.”17

1941: Series E Defense Savings Bond

When the US began to get involved in World War II in 1941, President Franklin D. Roosevelt announced the new Series E Defense Savings Bond. It was also known informally as Defense BoH Bonds. When it became available to the public the next day, Roosevelt purchased the first such bond from Treasury Secretary Henry Morgenthau.

After the Pearl Harbor attack, the Defense Bonds became known as War Savings Bonds or War Bonds. War Stamps with small denominations of 10, 15, or 25 cents were also issued so that every citizen could raise funds for the war.17

1955-1959: The Eisenhower Recession

From 1955-to 1959 came the “Eisenhower Recession,” in which long-term government bond investors lost massive funds. The impact of the recession spread across the borders of the United States to Europe and Canada, and many businesses went bust. Post-World War II, between 1945 and 1970, the worst recession led to a massive economic loss.18

A recession happened within the first few years when Dwight D. Eisenhower began his presidential recession term in 1953. It also coincided with the end of the Korean War.

As the inflationary pressure mounted during the second half of the 1950s, the Fed began to gradually shift their monetary policy from an “active ease” mode during the recession to one of “restraining inflationary developments.”

Despite the recession, Treasury yields were already on a longer-term trend higher. When the Fed initiated Operation Twist at the beginning of 1960, long-term bond yields were capped. Once these operations finished, yields continued to go upwards after the growth and inflation picked pace in the 1960s.

1963: The Introduction of the Eurobond

In 1963, Autostrade, the Italian national railroad operator, introduced the first Eurobond. A Eurobond is a debt instrument denominated in a currency different from the home currency of the country it is issued in.19 They are also called external bonds.

It was a $15 million bond (60,000 bearer bonds at $250 each) that the London banker, S. G. Warburg, designed and issued at Amsterdam Airport Schiphol. These Eurobonds were paid in Luxembourg. Initially, Eurobonds were delivered physically to investors, but today they are issued electronically.

Euro bonds were created in response to the imposition of the Interest Equalization Tax in the United States. The goal of the tax was to plug the deficit in the balance of payment in the country by lowering the domestic demand for international securities.

1969: Vietnam War Long Term Bond Losses

In 1969, the U.S. economy was dealing with rising inflation and interest rate. This was the same time at which the US began to get involved in the Vietnam War.

Long-term bonds were hit worst and lost almost 25% of their value that year. The Vietnam war was primarily funded by a hike in tax rates and an expansive monetary policy, which led to inflation.20

1970-1980: Introduction of Junk Bonds

In the 1970s and 1980s, there was a rise in high-yield corporate bonds primarily due to fallen-angel companies. These companies issued investment-grade bonds as they saw a massive drop in their creditworthiness. This dropped to a BBB rating, the lowest for investment-grade bonds.21

These fallen-angel companies could issue corporate debt after investment bonds suffered deep losses after two oil shocks, rising inflation, and accelerating interest rates. The interest payments on these bonds were not so attractive. However, their yields were quite impressive as they were priced in cents.

In the 1980s, these high yield bonds, also known as the “junked bonds,” boosted the appeal for leveraged buyouts (LBOs) as a funding mechanism through mergers.

The practice became rampant, and all kinds of investors turned to speculative-grade bonds as the preferred mode of financing. The bond market gradually evolved into a refinancing mechanism for bank loans. By 1983, over one-third of all corporate debt was a non-investment grade. The junk-bond market surged to $189 billion by 1989.

1994: The Great Bond Massacre

To deal with the stagnancy of the bond market, the Federal Reserve hiked interest rates for short-term funds in 1994. In February 1994, the Fed interest rate was 3%, which was too low historically. The Fed didn’t raise rates for six straight years in a row. Therefore, it increased interest rates to 3.25% and 3.37% in March and April. The rate reached 4.75% between May and August. This continued, and by December 1994, the Fed Funds rate reached 5.5%.22

This spurred a lot of skepticism in the market and sparked a sell-off rally. There was a global panic, and yields shot up from sub-6% to over 8%. According to estimates, the loss in the bond asset market during this financial crisis in 1994 was nearly $1.5 trillion.

2002: The Rise of Collateralized Debt Obligations

2000 saw the emergence of Collateralized Debt Obligations. These are not pure bonds but asset-backed securities. CDOs are structured financial instruments that buy and create a financial asset pool that includes riskier tranches of mortgage-backed securities.

The CDOs are a successor to the mortgage-backed securities created by Ginnie Mae and Freddie Mac in 1971. However, they didn’t see much activity until 2000.24

Another story states that the former investment bank, Drexel Burnham Lambert designed the earliest form of CDO in 1987. The bankers constructed the early CDOs by forming a collection of junk bonds that different companies issued.

After which CDOs became more popular, but they also became more complex and riskier. They were initially developed as instruments for the corporate debt markets, but post-2002, CDOs transformed into a medium for refinancing mortgage-backed securities.

These securities often hold high credit ratings, though. In 2002 and 2003, CDOs faced a setback when rating agencies downgraded several such securities. The volume picked up after 2003, though, and the sales increased tenfold. However, After the subprime financial crisis in 2007-2008, CDOs were considered one of the worst-performing instruments.23

The Bottom Line

The bond market is an integral part of the financial markets and will continue to act as a barometer of economic health and business and consumer sentiment. The opportunities for bond investors will increase with the return to economic growth and variation in the fixed-income market.

According to Morgan Stanley, in times to come, Investors are likely to see fixed income opportunities in five critical areas-High Quality Fixed Income, Lower-Quality High-Yield Bonds, Securitized Assets, and Emerging Market Debt, Convertible bonds.25

Sources: 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 25, 26, 27